Retirement Protection Plus (RPP) is not a pension plan, qualified retirement plan, or a qualified individual retirement account, nor a substitute for one. Rather, it is a program that provides disability income insurance to replace retirement plan contributions made by you and your employer in the event you become totally disabled. The Retirement Protection Plus Program is available for this specific purpose and is issued with the Provider Choice IDI policy having the same base policy language and Non-Cancellable & Guaranteed Renewable provision.

| Need For Retirement Protection Plus (RPP) Coverage |

| How Retirement Protection Plus (RPP) Works |

| Retirement Protection Plus (RPP) COLA Rider |

| Retirement Protection Plus (RPP) FIO Rider |

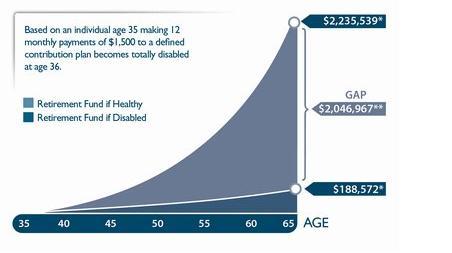

Need For Retirement Protection Plus (RPP):

If you became totally disabled, even if you had adequate group plus individual disability protection that would pay benefits to 65 or 67 would you be able to still put money away to save for retirement? Chances are you would likely need all of your disability benefits to live on since your disability benefits are likely going to be less that your pre disability after tax earnings. Additionally, if you are no longer working for a company because of disability, your former employer would not be able to put money into your retirement plan, even if they wanted to, because you are no longer an employee.

A long term disability can reduce the contributions into the retirement account resulting in less funds you have in retirement. This may resulting in you having a reduced retirement lifestyle from what you may have planned.

How Retirement Protection Plus (RPP) Works:

You are eligible for benefits when you are totally disabled and not working (modified own occupation). An option of Two Year True Own Occ is available on a stand alone policy. Once eligible for benefits, a monthly benefit up too 100% of your retirement contributions selected at time of purchase, including any employer-matching contributions, will be paid into an irrevocable trust. The trustee invests the benefits at your direction. The benefit period must be to age 65 and benefit periods available are 180 or 360 days.

Retirement Protection Plus (RPP) COLA Rider:

The COLA riders available under the RPP program are the same as it is on Provider Choice as long as the RPP coverage is issued as a separate policy vs being added to another Provider Choice policy as a rider. The cost of living riders adjust your policy's monthly benefit annually to help keep pace with inflation during a disability. They include annual adjustments and a minimum benefit adjustment of 3%, calculated on a compounded basis. Additionally, should you recover, you'd automatically retain increases, free of charge, until age 65. With many carriers, the increases are Consumer Price Index tied (CPI) and you must pay for any increases in coverage to keep upon returning to work.

Retirement Protection Plus (RPP) FIO Rider:

The FIO rider is the same rider available on other Provider Choice policies. This rider helps protect the ability to purchase more disability protection as your retirement contributions increase without having to show evidence of insurability. Here how it works:

Retirement Protection Plus is not a pension plan, qualified retirement plan, qualified individual retirement account, or a substitute for one.